Ask a UK business owner about the economy and you'll hear one story. Ask about their own business and you'll hear quite a different one.

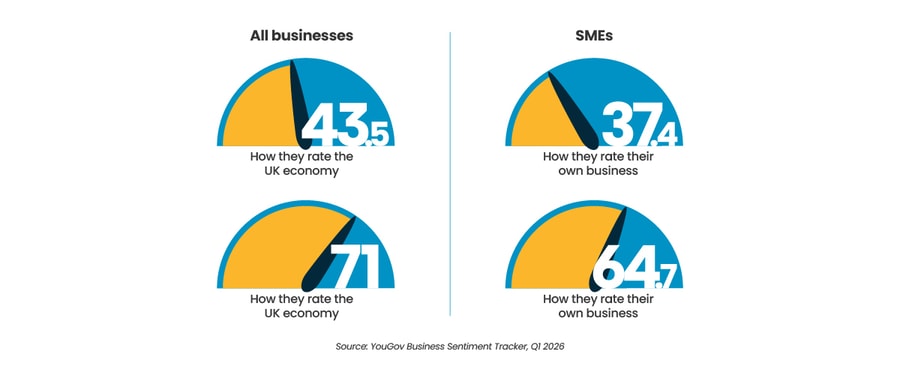

The YouGov Business Sentiment Tracker for Q1 2026 puts overall business confidence in the wider economy at just 43.5 out of 100. Among SMEs (small and medium-sized enterprises) it's even lower – 37.4. Given everything that's happened over the past few years, it’s not hard to understand why.

But ask those same businesses how they feel about their own prospects over the next 12 months, and something changes. The number jumps to 64.7 for SMEs – and 71 across businesses of all sizes.

That gap – 27 points between how bleak things look out there and how determined businesses feel about their own future – is what researchers have started calling the 'confidence gap'. And it tells a more interesting story about UK SMEs than the headlines usually give them credit for.

They're not waiting for the economy to feel better before they plan to grow. Instead, they're operating carefully – costs and interest rates are the primary concern for 56% of decision-makers, financial resilience is an active priority for 39% – but more than half are still focused on growth over the next 12 months. The intention is intact.

So why aren't more of them doing something about it?

From fear of funding to permanent non-borrowers

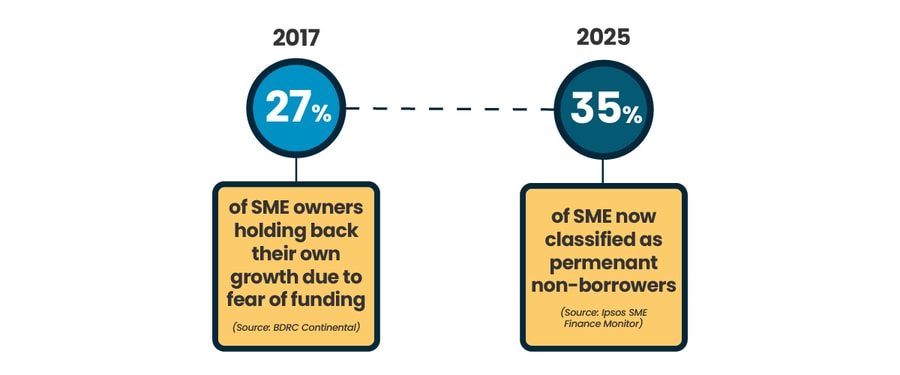

In 2017, a study by BDRC Continental found that 27% of UK SME owners were actively holding back the growth of their own business by refusing to take on external finance. Not because they'd been declined or couldn't find a suitable product. But because of what had manifested into a psychological barrier: the idea that needing funding was something to be ashamed of.

Nearly half of those surveyed believed British businesses were missing out on opportunities because of a collective reluctance to borrow. 45% felt the economy itself was being held back as a result. They could see the problem clearly in others – they just couldn't quite bring themselves to do anything differently themselves.

That was eight years ago, and the problem has only become more ingrained.

The Ipsos SME Finance Monitor, which tracks nearly 17,000 UK businesses annually, now identifies 35% of UK SMEs as ‘permanent non-borrowers’. In other words, firms with no external debt or credit lines that have made an active, intentional choice not to engage with lenders at all. This has developed from what was once just a fear into a posture. A settled position that a significant proportion of British businesses have adopted and show little sign of moving away from.

Put that figure alongside the YouGov confidence data and the contradiction is clear. More than a third of UK SMEs have structurally opted out of borrowing – at precisely the moment when those same businesses are rating their own growth prospects at above 60 out of 100. The ambition is there, but the follow-through isn't.

What the reluctance is actually costing

The British Business Bank estimates the UK's current SME funding gap at £65 billion.

That’s £65 billion in:

- Investment that isn't being made

- Equipment that isn't being bought

- People who aren't being hired

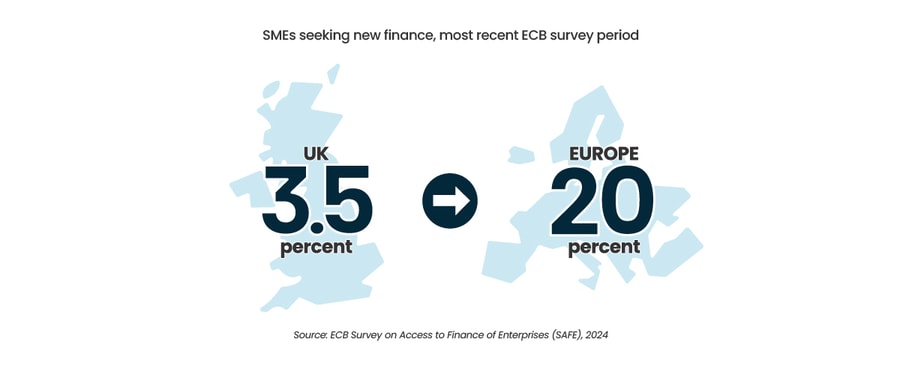

A survey by the European Central Bank (ECB) and the European Commission highlights the scale of the demand problem: only 3.5% of UK SMEs sought new or renewed finance in the most recent survey period, versus around 20% across the Euro area. British businesses are applying for funding at roughly one-sixth the rate of their European counterparts. A study highlighted by Financial IT found that 81% of SMEs had missed critical growth opportunities because they lacked or avoided external financing. The self-exclusion isn’t simply a personal choice, it’s having a direct and measurable cost.

Research by Juice found that 59% of SME founders who did try to borrow abandoned their applications mid-process – simply because the process felt too daunting to complete. And 72% of business owners who had previously been turned down said they were reluctant to ever apply again. All it takes is one difficult experience for the door to close.

And this reluctance is no surprise. Approval rates at the UK's largest banks fell to around 45% of applications in 2023, down from 67% before the pandemic. If you expect to be refused, and the process of being refused is time-consuming and demoralising, the choice to simply not bother starts to make sense. There's also a transparency problem: many lenders present their rates in unconventional ways, like factor rates or daily pricing metrics – "pay £50 a day" – rather than clear APRs, making it genuinely difficult for business owners to understand what they're being offered. Distrust, in some cases, is well-earned.

But the British Business Bank is explicit that systemic risk aversion – not just structural barriers – is one of the primary forces keeping small businesses from investing. And risk aversion compounds. The longer a business avoids borrowing, the more the idea of borrowing feels alien, and the more the reluctance calcifies into the kind of permanent non-borrowing the Finance Monitor is now tracking at scale.

The confidence gap and the funding gap are, at root, the same. Businesses back themselves – they just don't back themselves to the point of asking.

What businesses are actually borrowing for

For the businesses that do access funding, the data is instructive – both about what they're using it for, and about what it does for them.

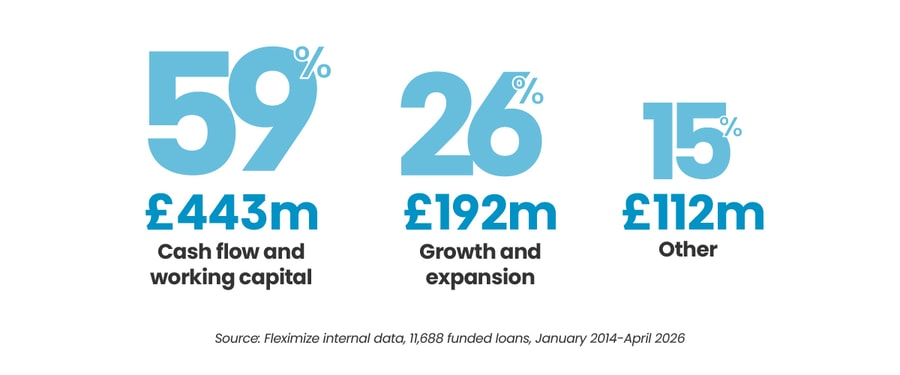

At Fleximize, we've funded more than 11,600 loans since 2014, totalling over £750 million deployed to UK SMEs. When we look at what those businesses were borrowing for, two purposes dominate:

- Cash flow and working capital accounts for 59% of funded loans – going directly into keeping businesses operational through uneven revenue periods, rising costs, and the kind of short-term pressure that can threaten an otherwise healthy business.

- Growth and expansion comes in as a firm second at 26%, investing in new premises, equipment, hiring, stock, and contract fulfilment.

More than eight in ten loans are going towards either keeping a business moving or actively growing it. Rather than borrowing out of distress like you might expect, they’re using funding the way it's supposed to be used – as a tool, instead of a lifeline.

Behind those numbers are real businesses making practical decisions.

- A recruitment group used a £210,000 loan to hire new staff and expand operations

- A convenience store owner in Coventry took £31,500 in working capital to grow and better serve their community

- A Swansea nightclub borrowed £50,000 unsecured to open a second location

- An award-winning bubble tea brand needed £157,000 to purchase a kiosk for a new site

The businesses behind these examples asked to remain anonymous. That's not unusual – in our experience, it's the norm. And it rather proves the point.

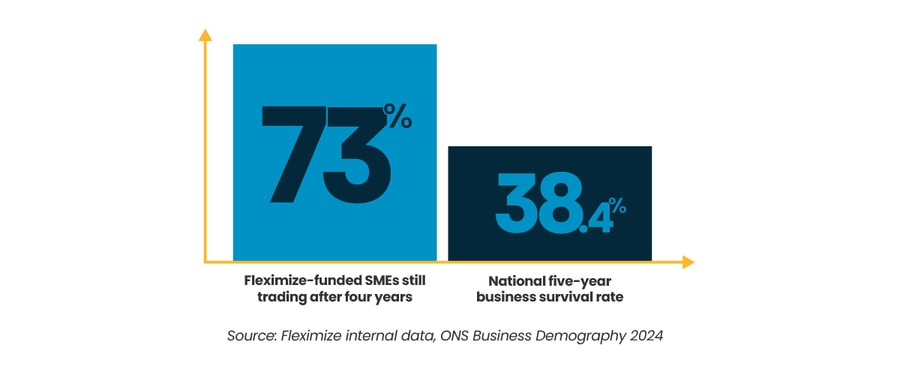

The outcomes matter too. Among Fleximize-funded SMEs, 73% were still trading four years after their first loan. For context, ONS data puts the UK's five-year business survival rate at 38.4% for businesses born in 2019 – fewer than two in five still active five years later. In other words, it’s consistent with what the wider research suggests: businesses that access the right funding at the right time tend to be more resilient, not less.

Around one in four Fleximize customers returns for further funding. Across recent cohorts, that return rate has been consistently above 30%. These are businesses that came in uncertain, borrowed, and came back. The anxiety, it turns out, rarely survives first contact with a lender who actually explains what they're doing and why.

Not all sectors are having the same conversation

The confidence gap isn't uniform. The YouGov tracker finds IT and Telecoms businesses among the most optimistic – buoyed by strong investment in AI infrastructure and data centres – while Legal, Hospitality, and Leisure sectors report the lowest confidence and the most acute economic anxiety. That's not surprising: the latter of these are also the sectors that bore the heaviest share of UK business insolvencies in 2023, a 30-year high. The confidence gap maps almost exactly onto which industries absorbed the most punishment from three years of cost shocks.

It's worth noting that access anxiety isn't evenly distributed within sectors either. The British Business Bank reports that Black and ethnic minority-led businesses face significantly higher barriers and lower confidence when approaching finance – a disparity that compounds the broader reluctance and means the funding gap falls hardest on the businesses that can least afford it.

A hospitality business faced with staffing costs and reduced footfall isn’t going to be having the same conversation as a tech firm driven by the current AI boom. One’s fighting to stay open; the other’s investing for growth. They don't have the same needs, the same risk profile, or the same relationship with the idea of borrowing. Treating them as the same borrower – with the same criteria, the same process, the same product – is part of how so many SMEs have come to feel that funding wasn't built for them.

The businesses that back themselves

The YouGov data captures something that anyone working closely with UK SMEs will recognise: the gap between how difficult things feel and how determined business owners remain. The macro picture is hard, but ambition at an individual level endures.

What the funding gap data adds is a challenge – not just to lenders, but to the broader conversation around business borrowing in the UK. "Funding" has become a word many business owners avoid. Not because the products don't exist or the money isn't there – gross SME lending hit £86.3 billion in 2025 (with £68 billion from banks and £18.3 from alternative lenders) – but because for too many SMEs, asking has come to feel like admitting defeat.

It isn't. The businesses that borrow strategically – whether that’s to manage cash flow, to invest in growth, or give themselves the headroom to operate without fear – are, as the evidence shows, more likely to still be trading four years from now than those that don't. The 35% of SMEs who have made permanent non-borrowing their default position aren't protecting themselves – they're limiting themselves.

With SME confidence in the wider economy at a multi-year low and a £65 billion funding gap still to close, the stakes of changing that conversation have rarely been higher. The businesses that back themselves deserve not only a funding market but a broader cultural narrative that backs them back.

At Fleximize, we've spent over a decade trying to be the kind of lender that makes asking feel less daunting. If you're weighing up funding options for your business, find out how our flexible loans work and what you could do with them, or explore your options.

A Guide to Internal and External Sources of Finance

— Read More — A Guide to Internal and External Sources of FinanceA Guide to Internal and External Sources of Finance

Every business needs money to grow, but where should you look? We break down the pros and cons of internal and external finance so you can make the right choice for your SME.

Does a Business Loan Affect Personal Credit?

— Read More — Does a Business Loan Affect Personal Credit?Does a Business Loan Affect Personal Credit?

Learn when your score might be impacted, how to protect it, and tips for separating personal and business finances.

Advantages of Loans in Business

— Read More — Advantages of Loans in BusinessAdvantages of Loans in Business

Discover the pros and cons of business loans, from quick capital to tax benefits – plus flexible funding options designed for SMEs.

These cookies are set by a range of social media services that we have added to the site to enable you to share our content with your friends and networks. They are capable of tracking your browser across other sites and building up a profile of your interests. This may impact the content and messages you see on other websites you visit.

If you do not allow these cookies you may not be able to use or see these sharing tools.